Executive Summary

Market Research

From Spending to Selection: How Saudi Consumers Are Redefining Value

PrizmData goes beyond numbers delivering insights & simplicity.

PrizmData goes beyond numbers delivering insights & simplicity.

Saudi Arabia has a particular way of holding tension. Over the past decade, the Kingdom has been reshaped by deliberate transformation. Vision 2030 has expanded opportunity, opened new sectors and shifted what many households believe is possible. That momentum has not disappeared in the face of regional uncertainty. It continues to sit alongside it.

That is the central insight of this research. Saudi consumers are stressed. They are more cautious with money. They are changing how they shop, how they eat out and how they approach larger purchases. And yet, at the same time, they remain broadly confident in their country, satisfied with government action and optimistic about their own future.

Those things are not contradictions. In Saudi Arabia, both are true at once.

Based on primary research conducted across the Gulf Cooperation Council between 20 March and 2 April 2026, this report looks at where Saudi consumers actually are today, emotionally, financially and behaviourally, and what that means for businesses trying to stay relevant in the Kingdom right now.

Start with the emotional picture, because it shapes everything else.

70% of Saudi consumers report feeling more emotionally stressed since the regional conflict began. The main emotions behind that stress are specific and widespread.

The numbers matter because they do not describe a small or isolated group. They reflect a majority experience, one that is sitting behind daily routines, spending decisions and conversations about the future.

And yet the emotional strain does not erase confidence. That combination is what makes the Saudi story distinct. In many markets, this level of stress would sit uneasily beside this level of confidence. In Saudi Arabia, they coexist within a framework of institutional trust that remains intact.

For brands, that distinction matters. Consumers are not looking for drama or for messaging that amplifies worry. They are looking for reliability, value and communication that meets them where they are.

One of the most revealing findings in the research is not just what consumers feel, but when they expect that feeling to matter.

72% of Saudi consumers believe the regional conflict will directly affect their daily lives within the next three months.

That is not a distant concern. It is an immediate one. It changes how people shop this week, not only how they think about next year.

The concerns attached to that expected impact are practical and direct:

Every one of these has a behavioural consequence. They influence mobility, spending, saving and how people choose to use their time.

Safety adds another layer of nuance. 72% feel considerably safe on a personal level, but the picture changes when family is brought into the frame. 69% feel more or slightly concerned about their family’s safety, which reflects how deeply family-centred the Saudi consumer mindset is. People are not only assessing their own risk. They are assessing risk on behalf of those they care about.

The three biggest sources of uncertainty are: regional, economic and personal stability.

These are not abstract worries. They shape how consumers think about the months ahead, and what they are willing to do now.

The financial shift emerging from this research is one of the most important signals for businesses.

Saudi consumers have not stopped spending. But they have changed their relationship with spending.

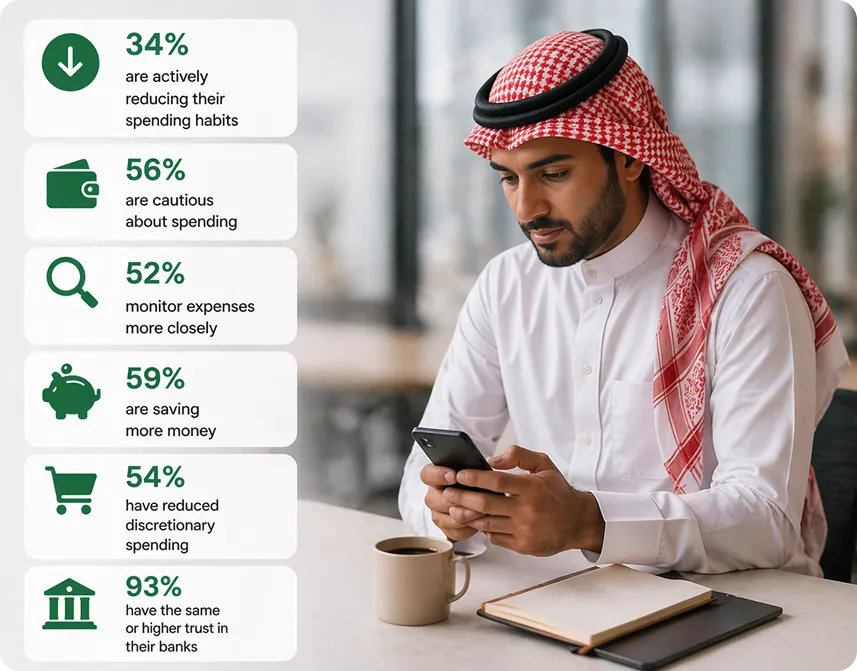

Preparedness is also visible in what consumers are already doing:

This is purposeful behaviour. It is not panic, and it is not passivity. Saudi consumers are running the household with more intent right now, deciding what matters, cutting what does not and building a buffer against uncertainty.

The confidence data makes that even clearer:

That is a crucial combination. Consumers have not lost faith in the system. They are simply engaging with it more carefully.

The clearest signs of caution are already visible:

This is not retreat. It is recalibration.

The macro picture becomes more useful when translated into category behaviour. Across groceries, food service, electronics and home furnishing, the same underlying logic plays out in different ways.

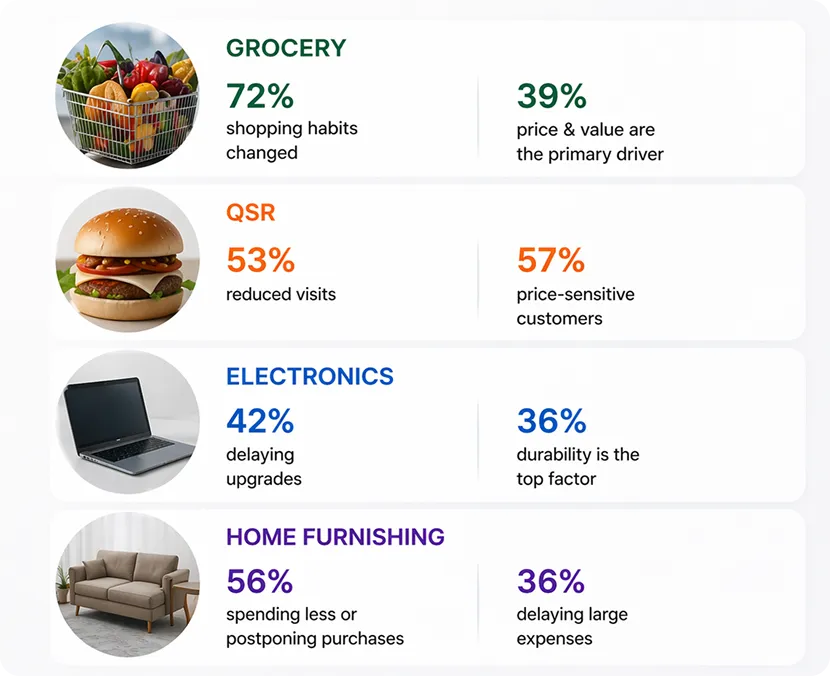

Grocery is where the shift is most visible. 72% of Saudi consumers say their shopping habits have changed, reflecting a move toward more controlled and practical purchasing. Consumers are making fewer trips (59%), focusing on essential items (43%) and actively seeking promotions (40%).

At the same time, the decision hierarchy has shifted. Price and value (39%) and availability (38%) now outweigh brand loyalty, which, while still relevant, is no longer the primary driver. A strong brand alone is no longer enough—products must be accessible and justify their price in the moment.

53% of Saudi consumers have reduced their visits to quick-service restaurants, but this is not a category in decline—it is one being redefined.

Among those still engaging, behaviour is shifting toward delivery (32%) and takeaway or drive-through (26%), with decisions increasingly shaped by budget (41%) and convenience (34%). Notably, 57% of consumers now identify as price-sensitive, and 42% are sticking to familiar choices rather than exploring new options.

The result is a more selective consumer, still active in the category but engaging on stricter terms—seeking value, familiarity and lower friction.

Consumer electronics are moving from aspiration-led to need-led purchasing. While roughly half of consumers report no change, a significant segment is becoming more deliberate—30% are less likely to buy or have postponed purchases, 42% are delaying upgrades, and 29% are waiting for discounts. A further 27% are only buying to replace essential items.

The decision framework reflects this shift: durability (36%) now leads, followed by price and promotions (29%) and brand trust (28%). Consumers are prioritising longevity and value over novelty, resulting in a more patient, considered purchase cycle.

Home furnishing and big-ticket purchases show the clearest pullback. 56% of consumers are spending less or postponing purchases, with many delaying large expenses (36%) or limiting purchases to essential items (30%).

This category reflects more than affordability—it reflects confidence in the near future. Large purchases are being deferred not simply due to price sensitivity, but because consumers are not yet ready to commit to longer-term spending.

For businesses, this signals that the barrier is not just value—it is reassurance. Addressing hesitation through flexibility, trust and consistency will be more effective than relying on discounting alone.

One figure stands above the rest:

93% of Saudi consumers report the same or higher levels of trust in their banks.

That matters more than it may first appear.

At a time when 70% are emotionally stressed and a majority are financially cautious, almost the entire consumer base is still maintaining or increasing trust in the financial system.

For financial institutions, this trust is an asset that needs to be reinforced. For every other business in the Kingdom, it is a signal that the market remains fundamentally sound.

The Saudi market right now is not one where standard playbooks apply.

The consumers businesses have been serving over the past few years, more aspirational, more experiential, more willing to trade up, are still here. But they are operating differently. They are asking harder questions and making more conditional choices.

That is where precision matters.

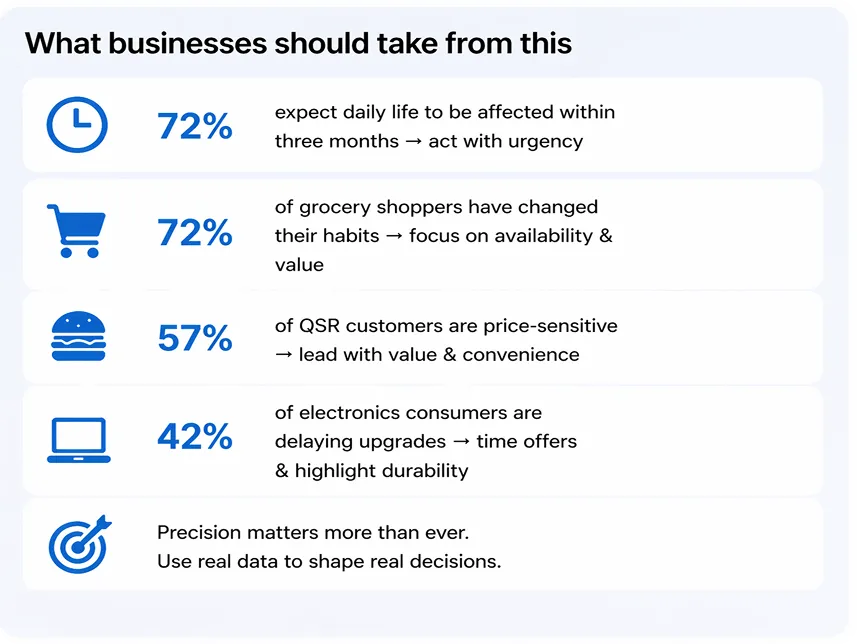

Knowing that 72% of consumers expect daily life to be affected within three months changes how urgently value-led messaging needs to be delivered. Knowing that 72% of grocery shoppers have changed their habits changes how retailers should think about assortment and availability. Knowing that 57% of QSR customers are price-sensitive changes what food operators need to lead with. Knowing that 42% of electronics consumers are delaying upgrades changes the timing and framing of campaigns.

None of this requires a total reinvention of strategy. It requires sharper reading of the consumer.

This research does not describe a consumer in retreat. It describes a consumer in transition.

Saudi consumers are still engaged with the market. They are still making decisions. They are simply doing both with a different set of priorities and a more deliberate mindset.

The brands that will come through this period strongest are not necessarily the loudest or the most heavily funded. They are the ones that understood the shift early, adapted clearly and showed up in a way that felt relevant to the consumer’s current reality.

That requires evidence over assumption.

It requires knowing not just what the headlines say, but what households are actually experiencing.

The data is there. The question is whether businesses choose to use it.