Executive Summary

Market Research

A Market Recalibrates: Kuwait’s Shift from Ease to Intentional Spending

PrizmData goes beyond numbers delivering insights & simplicity.

PrizmData goes beyond numbers delivering insights & simplicity.

Kuwait has always occupied a distinct position in the Gulf Cooperation Council. Its sovereign wealth fund, strong state institutions and one of the highest per-capita incomes in the world have historically given consumers a level of insulation that few regional markets can match.

But insulation does not mean immunity.

That is the central finding of this research. The regional conflict is being felt in Kuwait, and consumers are responding in ways that are both emotional and practical. Stress is rising. Shopping habits are changing. Big-ticket purchases are being delayed. Households are becoming more cautious with money. And yet, despite all of that, the wider consumer picture remains more measured than the headlines might suggest.

Based on primary research conducted across the GCC between 20 March and 2 April 2026, this report captures what Kuwait consumers are genuinely experiencing right now, how they are adapting, and what that means for businesses operating in the market.

The emotional response to the current environment is real. Nearly two-thirds of Kuwait consumers report feeling more emotionally stressed since the regional conflict began. The leading emotional states are Anxiety (54%) and Stress (49%), followed by a broader sense of unease that is working its way through households.

This is not a trivial shift. It suggests that the conflict is not just being observed from a distance; it is being processed in daily life, with consumers carrying a greater psychological load than before. That pressure shows up in moods, routines and decision-making.

And yet the mood is not one of collapse or panic.

67% of consumers feel confident in Kuwait’s ability to manage uncertainty, and a majority say they feel safe living in the country. Personal optimism is also holding up better than the stress figures alone would imply: 64% feel positive about their personal situation over the next 6 to 12 months.

This is the key tension shaping Kuwait’s consumer sentiment today. Consumers are alert, emotionally affected and behaving more cautiously, but they are not fundamentally destabilised. They are adapting, not disengaging.

For brands, that distinction matters. Messaging that pushes fear too hard will feel exaggerated. Messaging that acknowledges the pressure while reinforcing calm, reliability and value will be much more effective.

The data on safety reveals a nuanced, layered mindset. On a personal level, 68% of Kuwait consumers feel considerably safe. But that confidence softens sharply when the focus shifts to family: 82% feel more or slightly concerned about their family’s safety.

That gap is important. It reflects the family-centred nature of Kuwaiti society, where personal reassurance does not necessarily extend in the same way to loved ones. It also reflects the emotional weight of watching a regional conflict unfold nearby. Consumers are not simply asking whether they themselves are safe. They are asking whether the people closest to them are safe, and whether the environment around them remains stable enough to plan ahead.

Three areas of uncertainty stand out above the rest:

These are practical concerns, not abstract ones. They affect how people move, what they buy, how they budget and how they make plans. The consumer is paying attention, and the attention is highly functional.

That sense of immediacy is reinforced by another striking result: 78% of consumers believe the situation will directly affect their daily lives within the next three months. The main concerns they associate with that impact are cost of living, safety, access to goods and emotional well-being.

This matters because consumers are not treating the situation as a distant geopolitical issue. They are treating it as something that could touch everyday life very soon.

Even so, the institutional backdrop remains steady. 69% report satisfaction with the government’s response, which provides an important floor beneath the anxiety. It suggests that although concern is elevated, trust in the system has not broken down. That confidence helps keep the market from tipping into a more severe state of uncertainty.

Perhaps the most consequential finding in this research is not simply that consumers are spending less. It is the way their entire relationship with money has changed.

Kuwait consumers are moving away from comfort-led behaviour and into a more deliberate, need-anchored mindset.

The headline number sets the tone: 92% of consumers say they are more financially cautious than before. Within that, 34% say they are much more cautious, and 58% say they are slightly more cautious. That is an almost universal recalibration across the consumer base.

The behavioural evidence supports the same conclusion:

These are not signs of disorder. They are signs of control.

What is especially notable is that this caution exists alongside continued confidence in the broader financial system. 63% still feel confident about their financial stability, and 94% report the same or higher levels of trust in their banks.

That combination tells an important story. Consumers are not panicking. They are not withdrawing entirely. They are recalibrating in a deliberate, considered way. They are choosing caution because it feels rational, not because they have lost faith in the financial structure around them.

For banks and financial brands, that trust is a major asset. For retailers and consumer-facing businesses, it signals that demand has not disappeared, but it has become more selective and more conditional.

The financial caution described above is already visible in category-level behaviour. Across everyday and discretionary spending, consumers are becoming more selective, more price-aware and less influenced by aspiration alone.

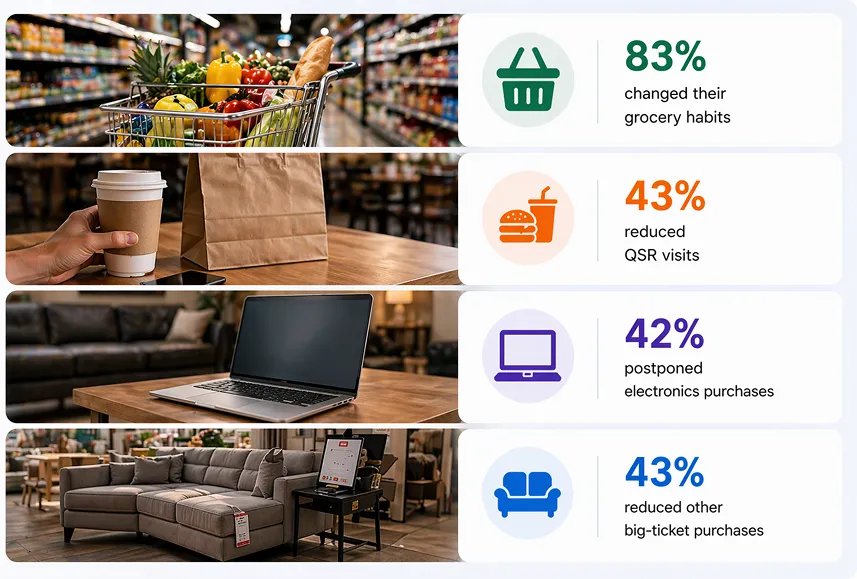

Grocery shopping shows the most obvious shift in behaviour. 83% of consumers report that their shopping habits have changed. Among them, 58% are making fewer trips, consistent with bulk-buying behaviour. 48% say they are buying only essential items, while 37% are actively stocking up on key goods.

Purchase drivers in this category are changing too. Availability (31%) and price/value (30%) now outrank brand as the key decision factors. That means brand loyalty is under pressure, and households are making more functional choices based on what is available, affordable and practical at the moment of purchase.

Quick-service restaurants are also feeling the shift. 43% of consumers have reduced their visits. Among those still ordering, delivery (32%) and takeaway (22%) are gaining share over dine-in.

The main drivers behind food-ordering decisions are now budgeting (32%) and convenience (26%). In addition, 68% of consumers self-identify as price-sensitive when ordering food.

That is a significant signal for food service operators. It means the category is still active, but the entry point for spending has changed. Consumers are not necessarily leaving the category; they are engaging with it more cautiously and with stronger expectations around value.

Consumer electronics are moving from desire-led purchase patterns to need-led ones. 42% of consumers have either postponed electronics purchases or say they are less likely to buy. Within that, 31% are specifically delaying upgrades, and 29% say they are only replacing essential electronics while waiting for discounts.

The main purchase triggers have shifted to:

This is a patient consumer profile. The appetite for electronics has not disappeared, but urgency has gone down. Consumers are willing to wait, compare and defer until the value equation feels right.

Home furnishing and large household purchases are experiencing a clearer pullback. 43% of consumers are spending less or actively postponing purchases, 35% are restricting themselves to only necessary items, and 31% are explicitly delaying large purchases.

This is the category most closely tied to future confidence. When consumers hesitate on home furnishing, it usually reflects a more cautious view of what lies ahead. In this case, that hesitation suggests households are not yet ready to commit to major outlays that feel too far removed from immediate necessity.

The data in this research tells two stories at once, and it is important to read them together rather than separately.

The first story is one of caution:

The second story is one of confidence:

These are not the numbers of a consumer base in retreat. They are the numbers of a consumer base that is adjusting its behaviour while still trusting the broader system around it.

That is why this moment should be understood as a recalibration, not a collapse.

Spending has not vanished. It has been deferred, reprioritised and made more conditional. The same consumers who are saving more and cutting discretionary spending today are likely to re-engage once conditions feel more stable and the emotional temperature lowers.

Consumer intelligence at this level of detail does more than describe market mood. It helps businesses make sharper decisions in real time.

Knowing that 92% of Kuwait consumers are more financially cautious changes how pricing and promotional strategies should be designed. Knowing that 83% have shifted their grocery behaviour changes how retailers think about assortment, availability and value. Knowing that 68% of QSR customers identify as price-sensitive changes what food service operators should communicate and how they should position themselves.

The opportunity is not to react broadly. It is to respond precisely.

Businesses that understand the consumer’s new mindset will be better placed to serve them through this period. That means being more relevant, more responsive and more grounded in the realities consumers are facing now, not the realities they were living with six months ago.

Kuwait consumers are not disengaged. They are engaged differently. They are asking different questions, paying attention to different signals and making different trade-offs.

The brands that recognise those shifts clearly will be better prepared both to serve customers during this period and to earn loyalty when conditions begin to normalise.

This research shows a market under pressure, but not a market in breakdown. Kuwait consumers are cautious, practical and emotionally affected, yet still stable in their core beliefs about institutions, banks and future personal recovery.

That combination of stress and stability is what makes the market so important to watch. It also makes it one where assumption is dangerous.

Through consumer sentiment research, primary research and interviews, businesses can replace assumptions with evidence and ground strategy in what consumers are actually experiencing today. In a market environment as fluid as this one, that is not a luxury. It is a necessity.