Executive Summary

Market Research

How UAE Consumers Are Navigating Uncertainty – Sentiment, Spending & Stability

Prizm Data goes beyond numbers delivering insights & simplicity.

Prizm Data goes beyond numbers delivering insights & simplicity.

Every morning, UAE consumers wake up, check the news, and make quiet decisions – what to buy, what to skip, what to save. These micro-decisions, happening across millions of households, are now being shaped by something bigger than personal preference: a region navigating visible geopolitical and economic uncertainty.

The ripple effects are real. Stress levels are rising. Shopping habits are shifting. Big purchases are being paused.

Yet something surprising emerges from the data – beneath the anxiety, there is a steady undercurrent of confidence. UAE consumers are not in panic mode. They are in planning mode.

This is what strategic consumer intelligence reveals when you look beyond surface sentiment. Based on a GCC-wide primary research study conducted between 20 March and 2 April 2026 by Prizm Data, this report unpacks how UAE consumers are truly feeling – and what that means for businesses operating in the region.

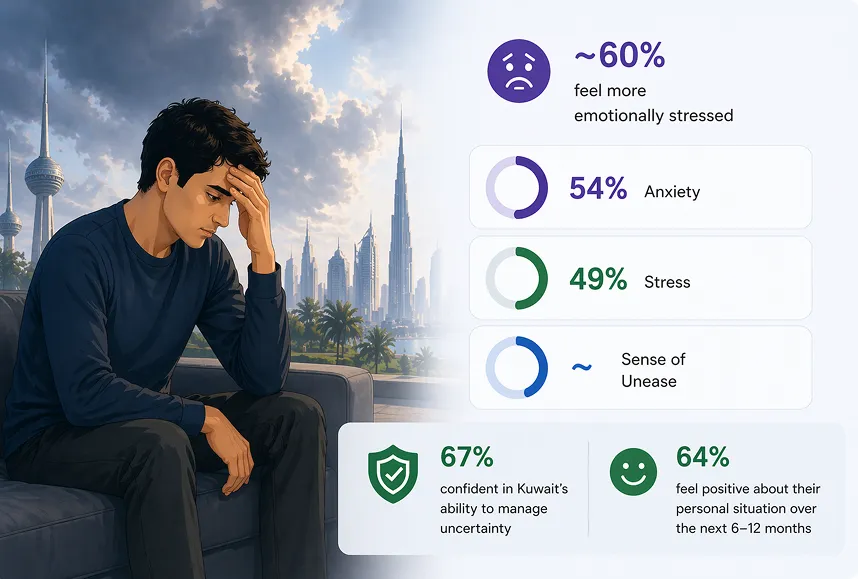

The numbers are hard to ignore. 68% of UAE consumers report feeling more emotionally strained in the wake of ongoing regional conflict. Stress (46%), Anxiety (43%), and Feeling Overwhelmed (37%) are the three dominant emotional states being reported.

And yet, the picture is not uniformly bleak. 75% of respondents still feel personally safe, and despite widespread concern for family wellbeing, only a minority describe their sense of security as having meaningfully deteriorated.

This tension – between emotional strain and personal stability – defines the UAE consumer mindset right now. It is a population that is acutely aware of external pressures but has not yet allowed those pressures to destabilise its daily sense of safety.

For brands, this distinction matters enormously. Messaging that leans too heavily on fear will feel out of step. Messaging that acknowledges difficulty while reinforcing stability and value will resonate far more deeply.

Perhaps the most significant finding in this research is not how much UAE consumers are spending – it is how they are spending. The data points to a decisive shift from spontaneous purchasing to deliberate, need-led decision-making.

71% say they are more financially cautious than before, with 27% describing themselves as “much more cautious.” At the same time, 54% feel confident about their financial stability – a number that reflects the UAE’s strong institutional foundations and the trust consumers place in them.

The behavioural patterns tell the same story:

This is not a consumer base in distress. It is a consumer base that has shifted its operating mode from growth to preservation – at least for now.

34% report an actual reduction in spending, while 50% report no change at all, suggesting the broader market remains more stable than headline sentiment might suggest.

The caution playing out in financial mindset is translating into very specific category-level behaviours.

What makes this research particularly instructive is the data that sits beneath the caution. For all the behavioural restraint, UAE consumers have not lost faith in the structures around them.

84% are confident in the UAE government’s ability to manage uncertainty. 80% remain optimistic about their personal situation over the next 6 to 12 months. 76% report the same or higher levels of trust in their banks.

These are not the numbers of a consumer base in crisis. They are the numbers of a consumer base that is recalibrating – deliberately, strategically, and with a longer horizon in mind.

For businesses, this signals a clear opportunity: consumers are not gone, they are waiting. The brands and services that demonstrate value, reliability, and relevance during this period of recalibration will be the ones that emerge with deeper loyalty on the other side.

Understanding consumer sentiment at this level of granularity is not just research – it is competitive advantage. Knowing that 71% are financially cautious changes how you price. Knowing that 80% of grocery habits have shifted changes how you range. Knowing that 84% trust the government changes the tone of your brand communication.

Through Consumer Sentiment Research and Primary Research & Interviews, businesses can move beyond assumptions and anchor their strategy in what UAE consumers are actually experiencing – right now, not six months ago.

These are not the numbers of a consumer base in crisis. They are the numbers of a consumer base that is recalibrating – deliberately, strategically, and with a longer horizon in mind.

For businesses, this signals a clear opportunity: consumers are not gone, they are waiting. The brands and services that demonstrate value, reliability, and relevance during this period of recalibration will be the ones that emerge with deeper loyalty on the other side.